I believe I have two main responsibilities when assisting my customers when obtaining a mortgage. First, to provide them the best possible mortgage product and terms available to them. Second, which may seem a bit strange coming from a mortgage loan officer, is my responsibility to help them eliminate this debt as quickly as possible.

I have done exhaustive research on every prepayment strategy I could find and wanted to share those with you so you could determine which one is best for you.

So much information and data is shared (in an easy to understand way) that you should never have to look anywhere else ever again to determine whether you should or should not prepay your mortgage and, if you do, which method is best for you.

My only fear is that you may get overwhelmed and stop reading, but I have worked very hard to make this fun and easy to read so you will enjoy it and be confident in what your plan is by the time you are done reading it.

Let’s get started…

First Things First

Before we jump into the various strategies to prepay your mortgage loan we must first cover the question of whether you should at all.

WHOA, wait a second! Ok, let’s be real for a minute. The mortgage industry is very heavily regulated with new laws and an entire new government entity called the CFPB which limits what we can and cannot say or do. Occasionally, you will be hearing from my attorney on certain disclaimers we need you to be aware of. So, here is the first one:

Scott’s attorney: Scott is not a financial advisor and cannot provide financial advice. All information provided is merely Scott’s opinion and you should seek advice from an independent financial advisor.

Back to what I was about to say before I was so rudely interrupted…I was going to tell you what I thought you should do before you start to prepay on your mortgage. Here is my quick list of steps to take prior to prepaying on your mortgage:

- Set up a an emergency fund. How much of an emergency fund should you have?? Suze Orman suggests 8 months of expenses. Dave Ramsey suggests 3-6 months.

- Max out your employer’s retirement matching program. If your employer offers a matching program for contributing to your retirement max that thing out. The rate of return you will get on that will normally outweigh any benefit of paying off debts. Just think if they give you $0.50 for every $1.00 you invest you just earned 50% on your money!

- Pay off credit card debt. The average interest rate for credit cards is normally in the range of 15%! Although some may disagree, based on how mortgages are amortized (we’ll talk about this later), I say pay off your high interest rate credit cards before you consider prepaying on your mortgage.

- Pay off other debts with rates higher than your mortgage. Do you have an auto loan? How about student loans? Is the rate higher than your mortgage rate? If so, pay those debts off first.

Have you heard of the debt snowball? Dave Ramsey made this famous. The idea is to pay off smaller balance debts first to create a snowball effect allowing you to gain momentum on paying off your debts. The debt snowball plan is great for feeling a sense of accomplishment but it is not the best mathematical plan to pay off debts. If you have not yet completed all the steps above and would like some help in determining which debts to payoff first, I highly recommend Vertex42’s debt reduction calculator. Within their calculator they provide you various debt reduction strategies auto-calculated for you to help you in determining the best method. The best method, mathematically is what they call the “Avalanche” which is paying off the highest interest rate debt first. Every time I have run it myself or have seen others run it the “Avalanche” method always produces the lowest amount of interest paid.

Mortgage Prepayment Strategies

Now that that is out of the way, and we can assume you have completed steps 1-4 above or you are just ignoring my advice (Hey, you get to do what you want to do!), we should look into the various options of prepaying your mortgage.

We should ask ourselves why we want to prepay or if we even should. What benefit do we get by paying off our mortgage quicker than we would with minimum payments? There are some tangible benefits such as less interest paid and lower monthly obligations. Some of the intangible benefits are a peace of mind that you do not have a mortgage, more security or decreased risk. Not everyone agrees that paying off a mortgage is what is best.

What if you took all the money you used to pay off the loan and invested it instead?

Is having a home owned free and clear better than having a cash position to pay it off really better?

These are great questions and questions I have asked myself. You could ask 10 different financial advisors and my guess is that you would get 10 different responses. The answer is “it depends.”

It depends on what the rest of your financial picture looks like.

It depends on the rate of return you are getting in the investment alternative.

It depends on how long you will be able to absorb any market fluctuations.

It depends on your risk tolerance.

It depends on your financial objectives.

I can say that I have considered the idea of splitting my residual income available to investing and paying off my mortgage. Is that the right thing to do? Maybe. Is it right for me? Well, right now it is.

Scott’s attorney: What is right for Scott is not necessarily right for you. You should seek advice from an independent financial advisor.

You are probably thinking, “On with it already…give me the strategies to pay off my mortgage!” You got it!

1. Bi-Weekly Payment Strategy

The bi-weekly prepayment strategy is one of the most commonly discussed strategies for prepaying your mortgage. Unfortunately it is also commonly misunderstood. Let’s make sure we are all on the same page on what the bi-weekly payment strategy really looks like.

Bi-weekly payments are payments made to and applied by the mortgage company every other week. Many people are paid every other week rather than twice a month or monthly so the bi-weekly payment strategy allows you to pay your mortgage at the same frequency you get paid. Let’s look at the numbers…

If you pay one full minimum payment every month you will end up making 12 payments at the full amount.

If you pay half of your monthly minimum payment every other week you will end up making 26 half payments or 13 full payments…or one extra payment each year.

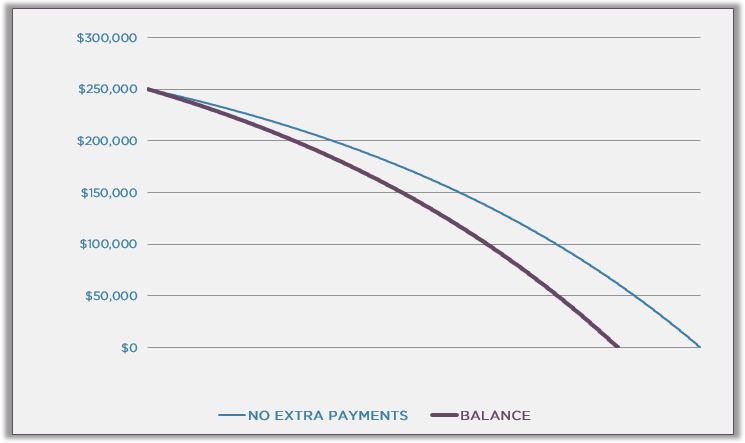

But the benefits go beyond just making one additional payment each year. By not only making your payments every other week but applying your payments at the moment they are received your mortgage balance decreases mid-month decreasing the amount of interest owed. This is a little confusing so let me show you some graphs that might help:

The top chart is what a normal amortizing mortgage loan balance looks like over time.

Scott’s attorney: Not every loan scenario can be shown and will vary based on loan amount and interest rate. For specifics on your mortgage seek the advise of a licensed mortgage professional in your state. The examples shown above are based on a starting loan amount of $250,000 with a 30 year fixed rate of 4.5%.

Pardon that little interruption! The next chart shows what the balance would look like compared to the bi-weekly payment plan assuming that the bi-weekly payments made are actually applied bi-weekly. What I mean by this is that the mortgage company is not just collecting your payment and holding until the full payment is made. Instead they are taking the payment and actually applying the appropriate amounts to both principal and interest therefore reducing your mortgage balance and reducing the amount of interest due at your next bi-weekly payment.

This is critical to receiving the highest benefit of a bi-weekly prepayment strategy. If the bi-weekly payment is not actually applied, the balance (nor interest) does not reduce mid-month. Some mortgage companies will not process mid-month (or bi-weekly) payments without additional fees, as that requires additional work for the mortgage company.

Scott’s attorney: For additional details on your mortgage contact your mortgage company to inquire about how they apply bi-weekly payments and if there are any additional costs to process multiple payments made each month.

If your mortgage company does not apply bi-weekly payments as they are made or you would prefer to not make payments every other week, the alternative would be to determine the extra amount to add to your payment each month to accomplish a similar outcome. To determine the amount of the extra payment you would take your monthly payment, multiply it by 13 (number of total payments that would be made if you were to follow the bi-weekly payment strategy) and divide by 12 (since you will be just making an additional principal payment with your normal monthly payment. Using an example here is how this would look:

Minimum Monthly Payment Due: $1,266/mo

Minimum Payment Multiplied by 13: $1,266 X 13 = $16,458

Total Amount of Payments Divided by 12: $16,458 / 12 = $1,371.50 (or an additional $105.50/mo paid each month)

Comparing the true bi-weekly payment strategy where payments are applied to the principal balance of the loan every other week and this plan where an additional principal payment is made each month we end up with more interest paid when the payments are made monthly, but not by much! Here are the numbers for you on a $250,000 original loan balance on a 30 year fixed rate of 4.5%

- Minimum Monthly Payments made Monthly: $206,018.21 total interest paid over 30 years (360 months)

- Monthly Payments made with an Extra $105.50/mo (1 extra payment per year): $171,416.07 total interest paid

- $34,602.14 saved compared to minimum monthly payments

- 25.67 years to pay off your mortgage or 52 months reduced off of your term compared to minimum monthly payments

- Bi-Weekly Payments: $170,601.18 total interest paid

- $35,417.03 saved compared to minimum monthly payments

- 25.58 years to pay off your mortgage or 53 months reduced off of your term ( compared to minimum monthly payments (just 1 month better than applying it monthly)

You decide – is it worth the extra work on your end to pay every other week (and possibly pay an additional fee to your mortgage company) or would it be simpler to calculate the amount and add a little extra to your payment each month?

2. Round-Up or Extra Monthly Strategy

We touched on this idea towards the end of the bi-weekly payment strategy. By manually calculating the extra payment needing to be made each month to accomplish the same outcome as the bi-weekly, we were following this strategy…applying a little extra to each monthly payment.

A common method of doing this is to round up your payment. For example, if your payment was $1,232 you might round up to $1,235 or $1,250 or $1,300 or even $1,500. Those are a few examples of how someone might round up the payments. The benefit of this method of prepaying allows people to budget easier. Rather than some random number calculated for the minimum payment you can easily round the payment up to better manage your day to day finances. In doing so you would pay off your mortgage faster than you would otherwise.

Using our same example from before at a loan amount of $250,000 loan amount at a 30 year fixed rate of 4.5% here are the numbers and charts to show how extra payments made monthly will impact the payoff of your mortgage:

$5 extra each month saves $1,982.97 in interest and reduces term by 5 months

$25 extra each month saves $9,514.19 in interest and reduces term by 14 months

$50 extra each month saves $18,120.57 in interest and reduces term by 27 months

$100 extra each month saves $33,108.00 in interest and reduces term by 100 months

$500 extra each month saves $98,992.58 in interest and reduces term by 157 months

$1,000 extra each month saves $132,787.44 in interest and reduces term by 217 months

Scott’s attorney: Examples shown above are based on a starting loan amount of $250,000 with a 30 year fixed rate of 4.5%. For specifics on your mortgage seek the advise of a licensed mortgage professional in your state.

3. Extra Payment Once per Year

Maybe you don’t have a lot of extra money each month to apply to your mortgage, but still want a strategy to payoff your mortgage early. About the same time every year there is an opportunity to apply a single extra payment. What time of year is that?? Tax time!

Maybe you get a bonus each year. Maybe you get a gift each year. Whatever the reason you have some extra cash laying around to apply towards your mortgage this would be the strategy for you.

Once again we will use a $250,000 loan amount on a 30 year fixed rate of 4.5% so we can see how this strategy impacts interest and term. I applied the extra payment every 12 months starting in month 6 of repayment:

$500 extra each year saves $15,394.71 in interest and reduces term by 23 months

$2,500 extra each year saves $58,377.90 in interest and reduces term by 90 months

$5,000 extra each year saves $90,176.99 in interest and reduces term by 142 months

Which Prepayment Strategy is Best?

I often read health and fitness blogs. Just like prepayment strategies there are numerous diet and exercise strategies you can choose. People are always wondering which diet is best. Which fitness program is best. Most of the time the response from the fitness professionals answer this with the same answer…

The best strategy is the one you will follow and stick with.

Alright, alright, I know this isn’t what you were looking for. I too like concrete answers to questions like “which is best”. Well, unlike a diet or fitness program there are mathematics behind the prepayment strategies and there is a “best” strategy. You might have already figured it out based on the data and charts I have provided to this point. To explain it I need to explain what amortization is and how it works.

What the Heck is Amortization?

Amortization simply means the method in which a debt is repaid over a period of time.

Mortgages are amortized in such a way that interest is front-loaded meaning you pay more interest at the beginning of your repayment than you do at the end. That is why you see a curved line in the charts. If mortgages were repaid with the exact same amount going towards the principal balance each month the line would be a perfect 45 degree angle down until the loan is paid off.

So why does this amortization thing matter to me?

In terms of a prepayment strategy amortization it makes all the difference. The sooner you pay down your principal balance the less interest you pay. Let me show you what I mean…

Going back to the Extra Payment Once per Year prepayment strategy we identified that paying an extra $2,500 extra each year saved $58,377.90 in interest and reduces term by 90 months if we paid this every year starting in month 6. This means you made an extra payment of $2,500 on month 6, 18, 30, 42, etc. If instead of waiting until month 6 to make the first extra annual payment if you were able to make it in month 1 (meaning payments on 1, 13, 25, 37, etc.) here is what happens:

From the chart you may not notice a difference, but by moving that annual payment from starting in month 6 to month 1 you end up with an interest savings of $60,224.70 and reduced term by 92 months as compared to minimum monthly payments. This means you would save $1,846.80 in interest and 2 months on your term just by moving the payments up from month 6 to month 1.

The Best Strategy

Putting all of this together what this means is the sooner you can make extra principal payments, the better. Instead of waiting until the end of the year to make an extra payment try to make smaller payments every month. If you receive an extra lump sum of cash that you can apply towards your mortgage don’t wait to put it towards your mortgage, do it on the next monthly payment you make.

Follow the four steps prior to prepaying on your mortgage. Identify the amount you can apply to your mortgage and how often you can apply the money. Make the extra principal payment as soon as you can and see the interest savings and months drop off the end of your mortgage!

Wouldn’t it be Nice?!

Wouldn’t it be nice if you could run all of these scenarios with your specific mortgage balance, interest rate, close date, and prepayment strategy?

What if you wanted to make an extra payment every other month?

What if you wanted to make an extra payment randomly?

What if your rate is higher…or lower?

What if you wanted to combine the strategies by making an extra payment every month and at tax time?

Well, you can! Vertex42 has a great tool I used for my calculations and charts. I’ve got great news for all you penny-pinchers out there trying to scrape together every last dollar to prepay on your mortgage – the tool is FREE! You can download it here.

Good luck! I would love to hear which strategy you plan to use and why. Leave your comment to share your experience with others!