You have a CreditKarma or FreeCreditReport.com account and you keep a close eye on your credit score. You receive alerts notifying you of any activity or score changes. You are on top of it! Keeping tabs on your credit score through subscription programs like this may be helpful to see what is going on but do you know how mortgage companies look at credit scores?

Did you know that some things you may be doing to increase your score may actually be negatively impacting your ability to qualify for a mortgage? Did you know that the score you see may be very different than the score your mortgage company sees?

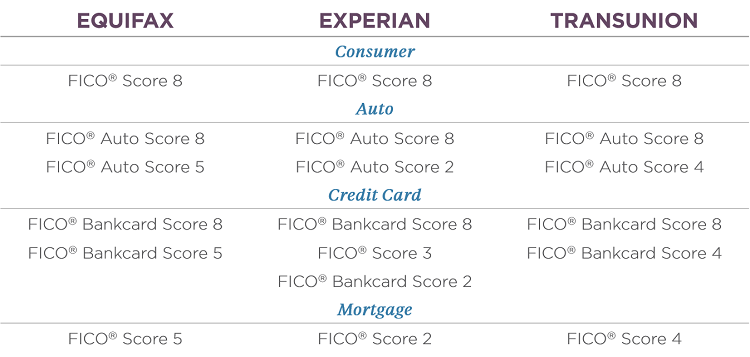

Your MANY Credit Scores

First things first. Let’s discuss credit scores. You would think that you would have just one credit score. But, in reality, you have many. You could have as many as four or six different credit scores!

Take a look at this chart:

What this shows you is the scoring models used by the three major credit bureaus (Equifax, Experian and TransUnion). Depending on the type of credit you are applying for a different calculation may be used to calculate your score. Notice that there is a consumer score, auto score, credit card score and mortgage score. In addition, each credit bureau may have a slight variation in their calculation compared to another credit bureau.

When you are monitoring your credit score or you pull your score through websites like FreeCreditReport.com you are receiving your Consumer Score. This score will be different than the score your mortgage company sees when they pull your credit.

In my experience, I have noticed that in most situations the consumer score is typically higher than the mortgage score. I guess it is kind of like vanity sizing in clothing stores. Did you know a size 34 pants today is actually bigger than a size 34 pants 30 years ago? Yep, they do that to make us feel better about ourselves. Well, same goes with consumer scores. The scoring model, from my experience, does the same thing. It provides you a score that is a bit higher than what the mortgage company sees when they pull their score.

Credit Scoring Models vs. Reality

Another trick used by some of the credit monitoring services is to use scoring models rather than actual scores.

Over time credit monitoring services or credit reporting agencies can get a pretty good feel for what will impact your credit score and by how many points. Rather than paying to pull your credit score every time you want to see what your score is they estimate what they believe your score is.

When you go out and apply for a credit card and an inquiry shows up on your credit your score will be impacted. The credit score monitoring service says you had a X point hit to your score. When they show this to you they are guessing. Sure, it is a very educated and calculated guess, but it is still a guess. Ultimately, you will not know the impact until a true credit report with a new credit score is pulled.

Mortgage Credit Qualifying

You finally decide to move forward and apply for a mortgage. You complete the application and a credit check is completed. Your credit report is pulled and you have a score. Well, you actually have three scores.

When mortgage companies pull your credit they typically pull, what is called, a tri-merge credit report. What this means is they are pulling a credit report from each of the three major credit bureaus and then compiling that into a single report with information from all three shown.

Representative Score

The mortgage company then looks at the scores available and based on the following criteria sets your representative score for qualifying:

- If all three scores are shown mortgage companies will use the mid credit score

- If only two scores are available they will use the lowest score

- If just one score is available that becomes your representative score.

Multiple Borrowers

When multiple people apply for a mortgage together there is an extra step to take to determine the representative score for the mortgage as a whole. The lowest of all individual representative scores is used for the mortgage.

Here is a quick example:

- Borrower A: 679, 682, 695 = 682 Representative Score

- Borrower B: 780, 792, 801 = 792 Representative Score

- Borrower C: 620, 622, 634 = 622 Representative Score

In this example if all three borrowers were qualifying together the representative score for qualifying as a whole would be 622 (the lowest of all individual representative scores). Now, if we removed Borrower C from the application and just qualified A and B on their own, the representative score would now be 682.

Score vs. Tradelines

Scores are important in qualifying and will be a factor in determining qualifying in general and in the interest rate and mortgage insurance rates you may received but it is not the whole story.

Tradelines are the accounts being reported on your credit report. They are the data behind the score calculation. Tradelines can be more important than your credit score.

Do you have any late payments?

How about any collections?

Are you close to maxing out your credit card?

These are some of the factors that play into determining your score and what the mortgage company looks at when determining what, or if, you can qualify for a mortgage.

Seek Advice

Credit scores and credit reports are confusing. One thing you might do to boost your credit score could have a negative impact on your ability to qualify for a mortgage. Depending upon your current motivations different actions should be taken to achieve the result you want.

If you are in the process of trying to buy or refinance a home and want to review your credit and position yourself in the best possible way, ask for help! Seek out the advice of a licensed mortgage professional who can help you in reviewing your credit and provide an individualized plan on what, if anything, you may need to do to manage your credit. Do not rely on general advice you can find online. Do not rely on the credit scores you pull yourself. You will need access to the tools and experience provided by a mortgage professional.

![Why I Like FHA Monthly Mortgage Insurance [FHA MIP EXPLAINED]](https://lendingahand.com/wp-content/uploads/FHA-MI-Explained-sm-768x432.jpg "Why I Like FHA Monthly Mortgage Insurance [FHA MIP EXPLAINED]")