FHA home loans have two types of mortgage insurance – up-front mortgage insurance premium (UFMIP) and monthly mortgage insurance (MIP). I’ve covered FHA monthly MIP in another post so the focus of this post will be on FHA’s UFMIP.

FHA up-front mortgage insurance is 1.75% of your base loan amount normally financed into your mortgage but can be paid in full at the time of closing so you might be wondering which way is best – find out how it impacts your loan amount, monthly payment and when you may be eligible for a refund of your UFMIP.

So, let’s get moving…

FHA Up-Front Mortgage Insurance Premium

FHA’s UFMIP is pretty simple and straightforward. It is just 1.75% of your base loan amount. But you can pay for this cost in one of two ways:

- Finance it into the mortgage

- Pay for it at the time of closing

What you are not able to do is split the cost up. This means that if you choose to finance the cost you must finance 100% of it into the mortgage. And if you choose to pay for it at closing you must pay 100% of the UFMIP at close.

Financing the UFMIP

Most people looking to obtain FHA financing for a home purchase choose to finance the UFMIP and the reason for it is simple…

FHA provides home buyers with one of the lowest down payment options available with a down payment requirement of just 3.5% and may even be combined with down payment assistance to lower the out of pocket expense even more. That means that FHA is generally attracting people looking for a loan option that requires less money out of pocket. The idea of paying an additional 1.75% at the time of closing is not something most home buyers would like to do, or even have the ability to do.

So, how does this up-front MIP impact your loan amount and monthly payment? Let’s take a look at an example:

Purchase Price: $300,000

Down Payment: 3.5% = $10,500

Base Loan Amount: $300,000 – $10,500 = $289,500

UFMIP: 1.75% = $5,066.25

Only full dollar amounts can be financed so the UFMIP is always rounded down to the nearest whole dollar amount when adding it to the full loan amount. Any amount remaining is added to the amount due at closing. In this example, $5,066 would be financed and the $0.25 would be added to cash required at closing.

Full Loan Amount: $289,500 + $5,066 = $294,556

Note: FHA has maximum loan limits which apply to the base loan amount which means your full loan amount may exceed FHA’s loan limits when you add the UFMIP.

Financed UFMIP and the Impact on Your Monthly Payment

When you finance the UFMIP you are not only incurring the cost of the 1.75% required by FHA but you are also paying interest on that money over the term of your mortgage.

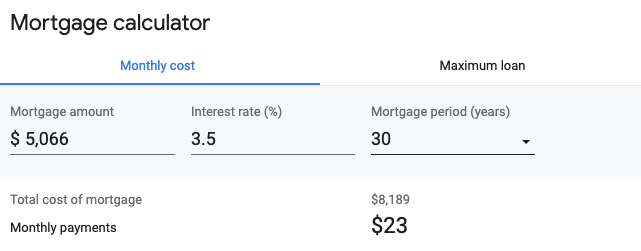

If we run a simple mortgage calculator on the $5,066 UFMIP from our example above using a rate of 3.50% (just a simple rate to use for illustration purposes) we can see that the impact to the monthly payment:

The $5,066 UFMIP with cost an extra $23/mo and will end up costing us $8,189 over the entire term of a 30 year mortgage.

Should You Finance the UFMIP or Pay it at Closing?

Now that you know the impact to you if you were to finance the UFMIP it is time to decide which option is better for you…

- Finance it into the mortgage

- Pay for it at the time of closing

Basically, it comes down to whether you have an extra 1.75% you can bring to closing and that amount of of your pocket is worth saving the few extra dollars each month on your monthly payment.

For most people, this is a quick and simple answer…finance it! That’s because the impact at closing ($5,066 in our example) is much greater than the impact each month (just $23/mo). Every time I’ve financed a home using FHA I have elected to finance the UFMIP rather than pay for it at closing. And during my career as a Mortgage Advisor over the past 20 years I think I have only had one client ever pay for it in full at closing.

Up-Front Mortgage Insurance Premium Refund

Did you know there may be a way to get a refund, or at least a partial refund on your UFMIP? Yep, and here’s how…

If you are doing an FHA to FHA refinance then you may get a partial refund back when you refinance. But it depends on how long you’ve had your FHA home loan.

You may be eligible to receive a partial refund of your FHA UFMIP when doing an FHA to FHA refinance within the first 3 years.

Here is the FHA UFMIP refund chart which shows you how much of a refund you may be eligible for:

| Year | Month of Year | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

| 1 | 80% | 78% | 76% | 74% | 72% | 70% | 68% | 66% | 64% | 62% | 60% | 58% |

| 2 | 56% | 54% | 52% | 50% | 48% | 46% | 44% | 42% | 40% | 38% | 36% | 34% |

| 3 | 32% | 30% | 28% | 26% | 24% | 22% | 20% | 18% | 16% | 14% | 12% | 10% |

You may have noticed but the first 6 months are greyed out. The reason for that is because you are only eligible for an FHA streamline refinance after 6 months. You can do a full FHA refinance within that time period but normally there would be no reason to do that. So, generally that means the maximum refund you’ll get when doing an FHA to FHA refinance would be 68% or less of the UFMIP amount you financed initially.

Calculating Your UFMIP Refund

Let’s look at a quick example. Let’s say you are doing an FHA to FHA refinance after 1.5 years. If we look at the chart we’ll see that would result in a 46% refund:

| Year | Month of Year | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

| 1 | 80% | 78% | 76% | 74% | 72% | 70% | 68% | 66% | 64% | 62% | 60% | 58% |

| 2 | 56% | 54% | 52% | 50% | 48% | 46% | 44% | 42% | 40% | 38% | 36% | 34% |

| 3 | 32% | 30% | 28% | 26% | 24% | 22% | 20% | 18% | 16% | 14% | 12% | 10% |

Using our example from before, we had a $5,066 UFMIP.

$5,066 x 46% = $2,330 refund

BUT…

You’re getting another FHA mortgage which means you have a new 1.75% UFMIP that must be paid for on this new loan. But, at least you’ll get that cost offset by the refund on your previous FHA mortgage.

So, there you have it. That is how FHA UFMIP works, how much it costs, the calculations to help you in deciding when to pay for it at closing vs financing it into the mortgage and how you may be eligible for a partial refund at some point in the future.

Related Videos

How to Find Down Payment Assistance Programs Where You Live: https://www.youtube.com/watch?v=ksQJO9BAdAM

What is Mortgage Insurance: https://www.youtube.com/watch?v=VaDReOwl6Nc

FHA vs Conventional 2020: https://www.youtube.com/watch?v=5BIIaQlOsis

🔴 Don’t forget to subscribe to our YouTube channel

Whenever you’re ready…here are some ways we can assist with your next home purchase:

📙 Download our Homebuyer Guide: Things to Consider When Buying a Home

🤑 Get the list of the No & Low Down Mortgage Options (in Colorado) so you can purchase your next home with less money than you thought possible

🚀 Want a boost in your credit score? Most advice about credit is generic or misleading and can hurt your home loan qualifying position. Take advantage of our Credit Booster Program and we’ll provide the exact steps you need to take to boost your credit score fast with a home purchase and mortgage pre-approval as the top priority!

⛰️ Want a pre-approval that makes buying a home easy? Find out how our Rock Solid Pre-Approval provides you with the confidence you can buy a home and are utilizing the best home loan option to do so.